What is mortgage insurance?

An introduction to mortgage insurance

If you don’t have a lot of experience with mortgages or the mortgage industry, “What is mortgage insurance?” is a big question to answer.Typically, lenders and investors require mortgage insurance for loans with down payments of less than 20%. The most common types of mortgage insurance options are provided by either:

- The Federal Housing Administration (FHA), which provides a program backed by taxpayers

- Private companies like MGIC, where mortgage insurance providers assume a portion of a lender’s or investor’s risk in making a mortgage loan, ultimately shielding taxpayers from liability

For that risk, the insurer collects a premium from the lender, who then typically recovers the cost of the premium from the borrower. The “risk” in private mortgage insurance is that a borrower may default on a loan, and that may ultimately result in the insurer having to pay a claim.

Private mortgage insurance is available on a wider variety of loan products and typically may be cancelled sooner than FHA mortgage insurance. FHA mortgage insurance is not cancellable, unless the borrower makes a down payment greater than 10%.

Private mortgage insurance is not mortgage life insurance, which pays off a mortgage if the homeowner dies or becomes disabled. It is not homeowners insurance, which protects homeowners from loss due to theft, fire or other disaster. Private mortgage insurance protects the lender and investor from loss, not the borrower.

How does private mortgage insurance work, in general?

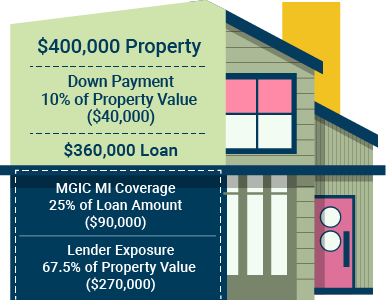

Consider borrowers who purchase a $400,000 property with a fixed-rate mortgage. They make a 10% down payment and are required to use mortgage insurance to finance a $360,000 mortgage.

Typically, on a 90% LTV, fixed-rate mortgage, investors require 25% coverage, meaning, in the event of a claim, the mortgage insurer is responsible for paying 25% of the outstanding loan balance, leaving the lender at risk for 67.5%.

On an uninsured loan, the lender is at risk for the entire loan balance.

If, down the road, borrowers fail to repay their mortgage, the lender or investor files a claim based on the unpaid loan balance, delinquent interest and foreclosure costs.

Borrower benefits

Financing with mortgage insurance creates opportunities for your borrowers.

Increased buying power

Because mortgage insurance makes it possible to buy a home with less than 20% down:

- Homebuyers – especially first-time homebuyers – can reach savings goals faster and become homeowners sooner than otherwise possible

- Move-up buyers are able to consider a wider range of homes and leverage their investment in their current home

Expanded cash flow options

Borrowers can benefit by putting less money down and keeping cash for other uses: making investments, paying off debt, or paying for home improvements or emergencies, for example.

Lower monthly payments

MGIC monthly mortgage insurance premiums are usually lower than FHA’s and do not require the upfront payment that comes with an FHA loan. That translates to lower monthly mortgage insurance costs and often monthly mortgage payments that are less than borrowers would receive with FHA financing. Learn more about MGIC monthly mortgage insurance premiums.

Secure, competitive, predictable monthly payments

A fixed-rate mortgage with monthly mortgage insurance provides borrowers with a locked-in monthly payment that will not increase and that will be reduced when mortgage insurance is cancelled.

Private mortgage insurance is cancellable

On most loans with private mortgage insurance, lenders must automatically cancel coverage when the loan reaches 78% of original value through amortization. Borrowers may be able to cancel private mortgage insurance by making extra payments to bring the loan below 80% of their home's original value. Borrowers may also request cancellation based on a new appraised value. When your borrowers are ready to cancel, they should contact their loan servicer for a full description of cancellation requirements. Learn more about cancelling mortgage insurance.

Private mortgage insurance is tax deductible for qualified homeowners

Beginning in tax year 2026, borrower-paid mortgage insurance premiums are tax deductible for homeowners who itemize and meet the income threshold. Borrowers should consult a tax advisor regarding mortgage insurance tax deductibility.

You might also like

-

-

Brush up on the basics

Read about ordering, activating and cancelling mortgage insurance.

-